Financial security is a key part of the American dream but that dream is becoming harder to achieve, especially for Latinos.

A recent report by policy think tank CFED found that despite positive economic growth and recovery, the racial wealth gap continues to grow. The wealth gap refers to the difference in net worth between white and non-white families. Net worth, or wealth, is the value of one’s assets minus their debts. Assets include your home, savings, retirement accounts, or any other item of value, including art and jewelry.

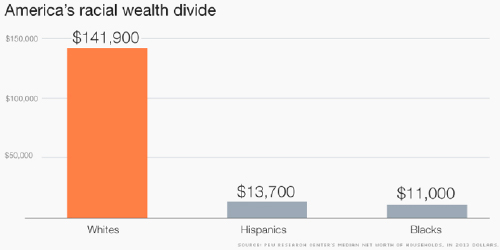

According to federal data, the median wealth for white families in 2013 was around $141,900, compared to Hispanics at about $13,700 and blacks at about $11,000. In sum, whites have 18 times more wealth than the average Latino family.

http://money.cnn.com/2016/01/25/news/economy/racial-wealth-gap/

According to Tanzina Vega of CNN, new data gathered by the CFED found that despite positive economic growth and recovery, the racial wealth gap continues to grow. There are many factors, including structural inequality, that contribute to the racial wealth gap, including wage disparities, intergenerational wealth transfer and access to financial services. Moreover, according to a Prudential report, Latinos are the least prepared for retirement and lag behind in emergency savings. While 44% of all Americans have less than three months worth of income saved, 67% of blacks and 71% of Hispanics lack adequate savings, compared to 34.7% of whites. Unfortunately, education alone does not solve the racial wealth gap. Nearly 60 percent of college-educated Hispanics surveyed report that is difficult for them to save for the future and cover personal expenses.

Despite these numbers, the good news is that everyone, at every income level, can makes changes to their personal finances that will help to improve their economic future. In fact, tax season, is the best time to take action because your finances are front and center. There is nothing like tax time to get your financial house in order, particularly since organization is the first step in taking action!

Financial planning is always overwhelming, so we put together a simple to follow 4-week #Financial360Challenge. Over the next 4 weeks we are going to help you take action on your financial future and build wealth for your family and community.

You can do it alone but it’s better with friends:

• Join Mi Dinero Mi Futuro’s Facebook group and share your progress and get your questions answered.

Tweet

I just joined the Mi Dinero #Financial360 Challenge #LoveYourLife @ModernLatinas

• Don’t miss our Financial 360 Challenge Twitter Party on 3/31 @9 p.m. (EST) for a chance to win free gifts for those that complete the challenge!

Week #1 Get Organized with a Reality Check

• Gather all your financial documents in a folder or Dropbox (Bank Statements, Credit Card Statements, Paystubs, Investment Statements, etc.)

• Pull your Free annual credit report: https://www.annualcreditreport.com/index.action

• Download Mi Dinero’s Financial 360 Workbook Calculate Your Net Worth

Week #2 Prioritize Budgeting & Emergency Savings

• Use your bank statements or Mint.com to review your spending habits for the last 2-3 months and set up your budget or refine it using our Financial 360 Workbook (*know your weekly spending number)

• Review your bank and credit statements for subscriptions and get rid of any you don’t use.

o Review your cell phone bill for any cancel any services you don’t need

• Automate your payments using your bank’s system to make sure you don’t miss a payment (this also helps to improve your credit score).

• Most importantly, set up an emergency savings account and aim to put aside at least 3x your monthly expenses, but start with an initial goal of at least 1x your expenses! Set this up so that it comes directly out of your account every month. Digit is also a helpful way to start saving. Remember budgeting will help you reach this goal!

Week #3 Improve Your Credit Score and Pay Down Debt

• Review your credit report for any old debts (generally after 7 years) or any suspicious activity. Also pull you credit score (free credit score with Mint.com or Capital One Credit Cards). You should aim for a credit score in the 680-720 range.

• Increase the credit limits on your current cards – not to use! – but to improve your credit utilization rate (see Financial 360 workbook to calculate your credit utilization)

• Make a plan to pay down high interest debt first by determining the amount you can pay every month.

Week #4 Get Serious About Your Retirement Plan

• Saving for retirement is critical for building wealth. The key is time, the longer you save, the more compound interest works in your favor!

• If you already have a 401(K) through your employer:

o Make sure you are maximizing your employer match-don’t leave money on the table

o Schedule a meeting with your advisor to check on your portfolio (a.k.a. portfolio rebalancing)

• If you don’t have a 401(K), don’t worry, you can open an IRA (ROTH IRA’s are a good choice for millennials) and can be opened easily on-line through Betterment or Wealthfront.

Last but not least, Sign –Up for early access to Mi Dinero Mi Futuro’s free personal finance platform.

Ramona Ortega is a former corporate lawyer and founder of My Money My Future, a mission-driven financial tech company that combines tailored content and simple to use tools to help Millennials, particularly young women and minorities, manage their money with confidence. MMMF’s personal financial management platform automates budgeting, guides Millennials through all their financial decisions and helps them choose the best financial products from a curated selection of partners. Ortega was recently named one of six Latina founders to watch and is on the board of the Latino Startup Alliance. She is a contributor to TechCrunch and Huffington Post on issues of law, tech and diversity.

One response to “Your Path to Financial Security #LoveYourLife”

[…] Originally published at Modern Latina […]